Venture capital (VC) funds play a critical role in the startup ecosystem, offering both capital and expertise to early-stage companies with high growth potential. Based on the sector, theme, or even risk-to-reward ratio, various funds have different lifespans and stages. According to Pitchbook, a VC’s average lifespan is around 13.1 years, with funds taking longer to return capital.

Let’s look at the venture capital fund lifecycle across its stages.

- Formation

The lifecycle of any private equity fund begins with its formation. The fund is formed and managed by a VC firm or a group of investors who put their money together. The primary managers of the fund are known as the general partners (GPs), while those who contribute their capital to the fund are limited partners (LPs). Limited partners are typically high-net-worth individuals, institutional investors, or other entities with a large supply of capital.

- Creating a fund strategy

General partners develop a fund theme or target by identifying areas of the economy or industries that they believe have the potential for significant growth and innovation.

The fund aims to generate attractive returns over its lifecycle by creating a focused investment strategy or thesis. This thesis also guides the fund's investment decisions throughout its tenure. This could be driven by observing trends in technology, demographics, or consumer behavior.

Most funds must show their investment thesis to LPs before they get a commitment for a particular amount of money. LPs evaluate this investment thesis to decide whether to invest in the fund.

- Fundraising

GPs often set a target before beginning the fundraising process. They begin soliciting funds from LPs, who commit to allocating a portion of their capital to the fund. They may not, however, invest immediately. Finding the proper LPs who resonate with the fund’s strategy can take a few months.

General partners often have to build relationships with potential LPs, answer their queries, and give them a detailed understanding of the fund’s investment strategy. They also have to provide detailed information on the particular sectors the fund will focus on, together with proven track records of the GPs in managing previous funds. The fund is closed once the target capital is met and money from the LPs has been pooled together.

- Establishment

A VC fund can be established as a limited partnership after it reaches its target size. It is now ready to seek out new investment opportunities where the accumulated capital can be deployed.

- Investing

At the investing stage, fund managers find suitable avenues or investment opportunities and increase deal flow to deploy their capital. The investments are typically in early-stage companies with very high growth potential. To be considered, these companies should have an area of focus, sector, or theme that overlaps with the fund’s thesis or strategy.

- Deal sourcing

Deal sourcing is the initial phase of the venture capital life cycle, where GPs identify companies to invest in. Through personal or business connections, via pitches, referral networks, or alternative sources, fund managers find ideal companies to invest in. They aim to supercharge portfolio companies with capital, access, or expertise to generate superior returns. Once a company or start-up has been identified, the VC will begin the process of due diligence to assess the firm’s business model, growth projections, and market opportunities.

- Negotiation

VC terms and conditions, which range from the amount of capital deployed to the number of seats on the board, vary from company to company. GPs and start-ups negotiate based on their shared belief in the company's future. If both parties are amenable to the terms presented, the start-up gives up a portion of its equity in exchange for a fresh capital infusion, thus becoming one of the fund’s portfolio companies.

- Portfolio Management

Once a VC has successfully deployed its capital and added start-ups to its portfolio, through the tenure of the fund, the GP must balance the needs of various portfolio companies to help them maximize their value. Portfolio management consists of fund managers allocating resources effectively to provide every company with adequate support, from additional capital to hands-on intervention.

According to Shikhar Ghosh, a professor at the Harvard Business School, the failure rate for VC-backed startups is 75%. In other words, three out of every four start-ups fail and can never return the cash deployed.

Not all investments will generate returns, and fund managers must make harsh decisions to optimize returns for investors. This will also help mitigate certain risk factors. The portfolio management period is the longest in the lifecycle of a VC. Once the fund is nearing the end of its tenure, or if the GP believes that there is limited upside in continuing to remain invested in a portfolio company, the fund moves to exit its holding.

- Exiting

Finding an effective exit strategy is a critical part of venture capital investment, and VCs must be well-informed about their various options. There are several exit strategies that venture capitalists can employ when divesting their stake in a start-up, each with its benefits and drawbacks.

- IPO

One such exit strategy is the Initial Public Offering (IPO), which involves listing a start-up on the stock exchange. A successful IPO can provide VCs with significant returns on their investment as VCs enter a start-up at a much lower valuation

However, a study of 135 unicorns by the National Bureau of Economic Research found that many of them had inflated valuations before an IPO. Astonishingly, it found 15 companies that were overvalued by 100%.

- Mergers and acquisitions

The merger and acquisition (M&A) approach, where a larger company acquires a start-up, is another common exit strategy. Many large corporations seek to enhance their product offerings or expand their market share by purchasing highly adept start-ups. The sale of a portfolio company to a larger entity can yield significant returns to a VC while also providing the start-up with resources to scale up and compete globally. On the start-up side of it, however, an M&A often means giving up the dream of becoming a unicorn and being left to function under the regulations of a larger entity.

- Secondary sale

In a secondary sale, a VC usually sells its stake in a start-up to another investor. This often happens when there is no immediate prospect of an IPO or M&A, and the general partner or fund manager wants to disinvest. Sometimes, these sales can be an attractive exit option for VCs, while the start-up has the advantage of a new investor putting fresh capital into the firm.

- Share buyback

This happens when a start-up purchases its shares back from a VC, believing that the firm can perform independently without oversight or additional capital infusion. Share buybacks are beneficial for both the portfolio company and the VC. The start-up's most significant benefit is reclaiming its original ownership structure.

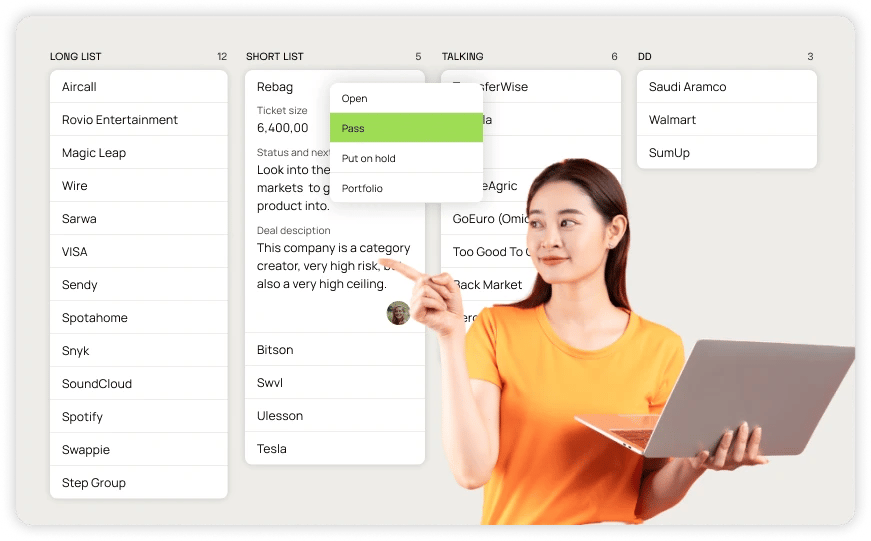

Simplify your investment process with Zaplow

The lifecycle of a VC fund may vary, but the key to maximizing returns is investing in the right start-ups.

Zapflow is a deal flow management tool that helps VCs capture and analyze data accurately. You can use it to communicate with founders, generate custom reports, and conduct analyses that help you simplify the process of finding the ideal start-up or founder to invest in.

Manage your pre- and post-investment workflows faster than ever by leveraging the power of data collection and boosting the effectiveness of your team,

Get in touch today!