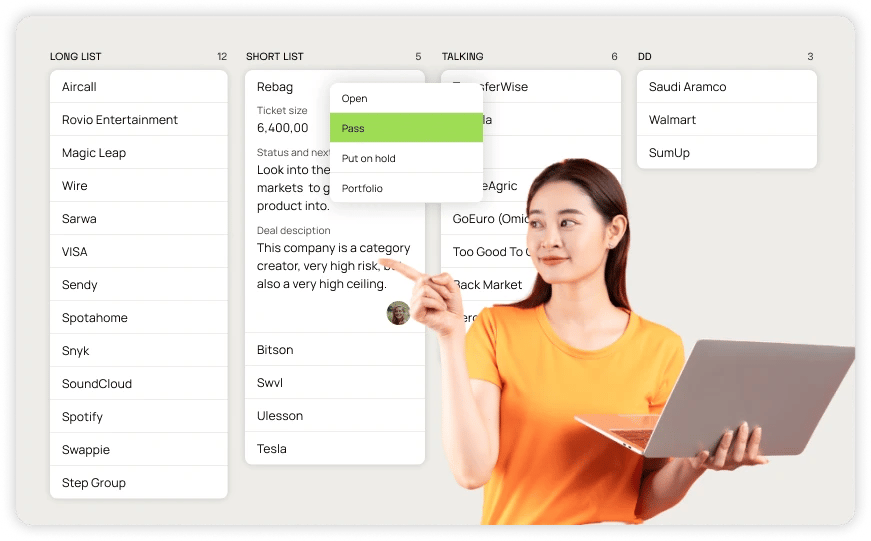

Finding the right deals is arguably the most important skill a VC is expected to learn and hone while working in the capital markets industry. A sizable VC firm handles hundreds of leads at any given time, and even more under viable market conditions.

The average firm considers over a hundred opportunities before finally investing in a promising startup. This tedious and highly selective investment process is the way VC markets operate. Investing in a startup is essentially a long-term commitment for a firm, one that costs them huge amounts of time and money. In some cases, entrepreneurs might even need to be coached to understand the inner workings of their industry better. This makes each VC deal a significant investment on the firm’s part, which makes it all the more important for it to assess each lead properly.

With the right tools and experience, VCs can learn to recognize red flags in the initial pitches. Spotting red flags early on saves you the time and effort it would take to carry out due diligence processes. It also allows you to reject unviable leads right at the outset instead of leading them on for months.

What are the most important red flags to consider before investing in startups?

A VC pitch can have several red flags that VCs need to be able to recognize. This includes both operational and philosophical pain points and financial concerns among other things. For instance, if a startup centered around being eco-friendly doesn’t fully plan on implementing green technology across its various departments, it will come off as fake and disingenuous to customers sooner or later.

So here are a few VC red flags that venture capital firms should always be on the lookout for.

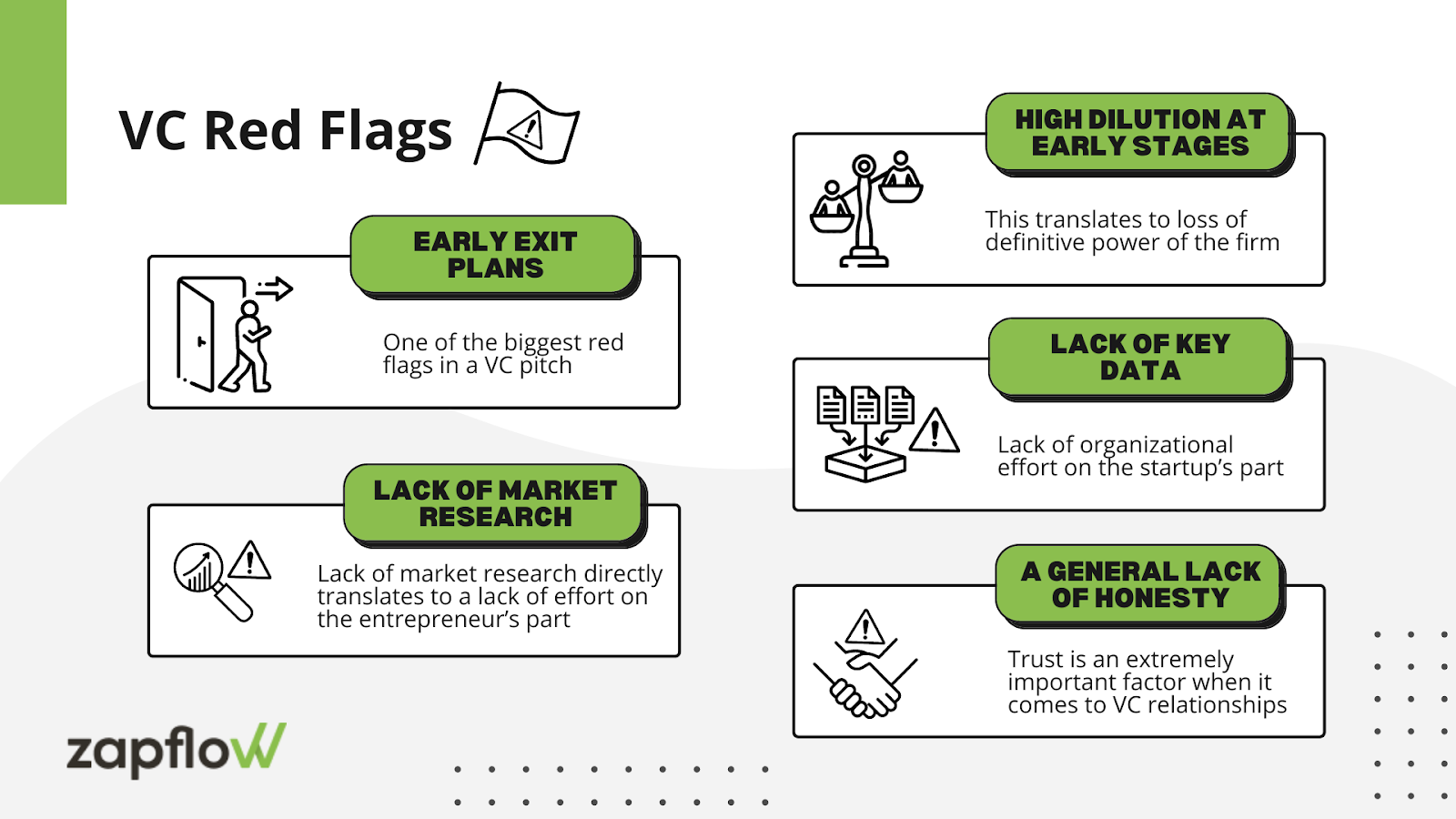

- Early exit plans

Having an exit plan already in place is arguably one of the biggest red flags in a VC pitch. This is especially true for founders who plan on selling their startups after a specific amount of time. Early exit plans show a lack of confidence or a lack of willingness to invest time and effort in an idea on the founder’s part. A founder who is underconfident in their own idea should always be a red flag to investment firms.

Early exit plans can also severely skew the vision a founder has for their company, which can lead to operational differences down the road. For example, a founder who is planning on selling their startup in a year or two will naturally be opposed to scaling up and foraying into new product categories, even if investors deem it to be the right move at the time. While exit strategies can be a part of contingency plans, it is important to look at them as a risk-management measure and not an ultimate goal when it comes to VC investment. Having detailed exit strategies already in place can be a cause of ideological conflict between entrepreneurs and VCs. This can potentially cost the firm a lot of time and money and may even mar its market reputation.

- Lack of market research

Market research is one of the key parts of any VC pitch. When conducted aptly, market research can inform investors of several important aspects like market landscape, target consumer demographics, long-term revenue projections, how competitive the sector is, and what a startup needs to do to set itself apart. When a startup puts organizational and financial structures in place, market research plays a huge role in determining what would be ideal for the startup and how it should structure itself to meet its long-term financial goals.

On the other hand, a lack of market research directly translates to a lack of effort on the entrepreneur’s part. Without apt research, it would be difficult for a startup to structure itself in a way that is conducive to businesses in their sector.

- High dilution at early stages

A higher-than-usual amount of dilution, especially in early funding raises, can be a cause of concern for VCs. Highly diluted startups pose several questions: ‘Will your firm be able to retain the necessary power required to make operational changes at the startup?’, ‘Can there be operational and philosophical conflicts with other investors?’, ‘Would the founders be motivated to opt for a profitable exit soon?’, and so on.

A highly diluted startup usually already has several investors on board, which directly translates to a loss of voting power for your firm. Not being able to make the right changes at the required time might lead to the startup progressing in a direction that isn’t necessarily in line with your goals. Further, the presence of several investors also means the presence of multiple investment philosophies, which might not all coincide with each other. This can lead to major operational and philosophical conflicts in the future. Veteran accelerator firm YCombinator has laid down these general guidelines to judge equity dilution in startups:

- Founders should only sell 10%-15% of their startups in the seed round.

- Equity dilution can go up another 15%-25% in the series-A round.

- Series A dilution should be limited to around 7% if an accelerator is involved.

- The total dilution (if one big funding round is being held) should not exceed 30%-40%.

It is important to know that these are simply general guidelines and not hard-and-fast rules that VCs are expected to follow. YCombinator itself proceeds to quote instances where founders retaining 50%-60% of their equity in their series-B funding round have gone on to be very successful. The amount of dilution that should be tolerable depends on your investment philosophies, future goals, and the particular startup being assessed.

- Lack of key data

The unavailability of important historical data like information about existing investors, previous funding rounds, projected revenues, and KPIs is a big VC red flag. When relevant data is not provided to a VC firm, it can be for one of two reasons.

The startup might not have properly cataloged information on its cap table about its existing investors and its funding rounds or it might be hesitant to share the data with you. Failure to maintain a proper record of financial and operational data suggests a lack of organizational effort on the startup’s part. Not paying enough attention to documentation and cataloging is a red flag that VC firms should actively avoid. On the other hand, if a founder is hesitant to share their data with you, it can be a sign of mistrust. When either party is not able to fully trust the other in a VC deal, it becomes very difficult to manage and mitigate conflict.

In either case, VCs miss out on important data required to carry out due diligence processes and generate a future roadmap for the startup. A lack of available data compels VCs to enter a deal more or less blindly, which leads to increased investment risks and much higher chances of failure.

- A general lack of honesty

Dishonest and opaque pitches constitute the biggest VC red flags. When a startup is not completely honest and transparent about its revenue projections, consumer base, and other investors, it sets a precedent that can ultimately lead to investment risks for the VC. Trust is an important factor when it comes to VC relationships. Both startups and VCs need to work together along multiple avenues to ensure the steady growth and complete operational health of a company. A lack of trust and transparency can hinder this, causing problems in the deal.

How to deal with VC red flags

Social capital is one of the most important assets a VC can have. Not only does it help you build a strong market reputation, but it also allows access to a quality deal flow. This makes it very important for firms to respond to pitches politely and cordially. When you spot a red flag in a pitch, you should present your reservations in the form of observations or constructive criticism. This can motivate the founders to view the problem from your POV and try to work out a viable solution. Timely and effective communication is important for all leads, even if you plan on rejecting them.

Zapflow is a state-of-the-art deal flow management software that can help you communicate with your startups quickly and effectively. Our single-pane-of-glass design helps organize all inbound communication in an accessible manner. This leaves VCs free to reach out to any of the leads and raise relevant concerns on the platform. All this saves you the hassle of scanning through lengthy email threads to list out the important points from an exchange between you and a startup.

Zapflow can help boost the productivity of your VC firms by organizing and analyzing your deal data through elementary, user-friendly processes.